Ravi Duggal is a sociologist, health researcher and activist associated with the People’s Health Movement. His work over the years has mapped trends in changing budgetary allocations in the health sector and the many ills of privatisation. In this interview with The Third Eye, he makes a compelling case for government intervention with appropriate regulation of the private sector, focusing particularly on the enigma that is health insurance.

This conversation took place in July 2021. An edited transcript of the interview follows.

If you had to start by summarising India’s approach to healthcare, what would be the highlights?

We have neglected primary healthcare all these years despite our National Health Policy, the first policy of 1983, which is the first time we came up with a health policy at all. There was some push towards strengthening healthcare after India signed the Alma Ata Declaration in 1978, to push for “Health for All” by 2000. That was the slogan of the World Health Organization (WHO). India came up with the health policy document because that was one of the requirements of the WHO agreement.

What were we thinking before 1983? What was going to be the imagination of health in India, which even then had very poor health indicators—high infant and maternal mortality, for instance? As a nation-building exercise, what was the role of health?

Whatever thinking was done in the country was done by the Planning Commission for all social sectors as well as the economic sectors.

They only developed programmes for firefighting. Since tuberculosis (TB) was a problem, let's have a National TB Control Programme. Leprosy was a problem, so we created a National Leprosy Eradication Programme. We never thought of it in a comprehensive way as something people need.

At least now, in primary health centres (PHCs), you do get some curative care. But in the 1960s and ’70s, curative care was practically absent. Medicines got only around 1% of the total PHC budget, which was certainly not sufficient.

Did this approach shift at some point?

The Minimum Needs Programme was started by Indira Gandhi in rural India under the Fifth and Sixth Five-year Plans. She knew that her constituency was rural India, and urban India was definitely not going to support her the same way. The target set was one PHC per 30,000 population. Within a period of three to four years, most states achieved that target, and you also see this in the spending on healthcare in the Sixth Plan period.

I think somewhere in 1987, we peaked in terms of healthcare spending. At about 1.6% of GDP, a lot of the funding went into the minimum needs programmes—strengthening the rural health infrastructure, trying to attract doctors, etc.

The same thing didn’t happen in urban India.

This seems to have been a decent start. When did things start going wrong?

With Rajiv Gandhi, we started opening up our economy. We became grossly indebted. We had to undergo structural reforms under the World Bank because our foreign exchange was depleted down to just 15 days of imports. In that scenario, economic reforms came in and they focused on reducing public expenditure. The axe fell first on the social sector—health, education and other welfare programmes.

There was this whole World Bank strategy also—its 1993 World Development Report focused on health and a very clear message came out of that: leave healthcare to the private sector. This was despite the World Bank's own studies showing that the private sector does not deliver on healthcare. It creates more inequities.

The World Bank very clearly pushed for insurance-based healthcare and pushed for private sector-strengthening in healthcare.

So, when does private health insurance come in?

Private health insurance started in India in 1986, but these were public sector companies that were doing it more as a kind of subsidy for public benefit. They were not making money out of it. Mediclaim policies that began in 1986-’87 had low premiums. The basic idea was to provide support to middleclass families and also to get them hooked on private care, especially for hospitalisation. They did not reach out to the poor.

Earlier, there had been various other ways of helping employees in terms of healthcare. People got monthly allowances for medical assistance, or there was some medical reimbursement built into the human resource (HR) policies of organisations. But then the employers realised that if we insure them, it would be a bulk deal for all employees together. The cost would be much less to the company because of volume. They negotiated the premium to bring it down for what is called group insurance policies. Even today, group insurance policies are about 40% of the total insurance sector, if you exclude the publicly financed insurance policies that the government pays for. So they encouraged employees to opt for insurance; the attraction was that without any pain, the middle classes could access private hospitals like Jaslok, Hinduja and Apollo.

It's only when insurance becomes a significant mechanism of financing, especially for the middle classes, that the latter ditch the public health system.

What about the public insurance schemes?

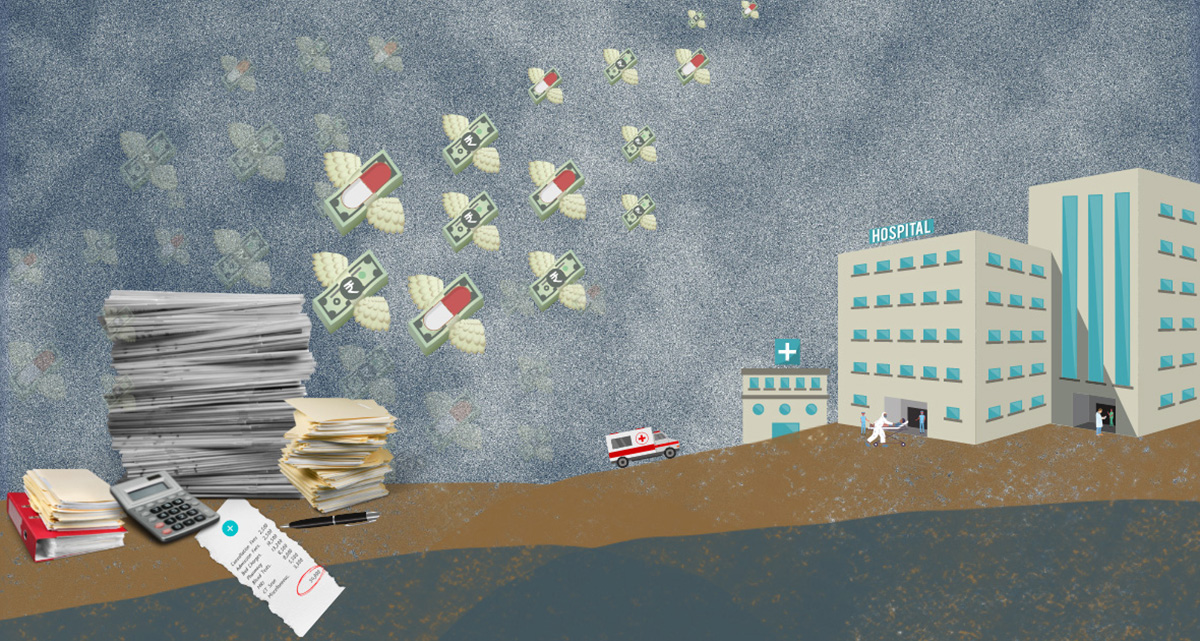

The Rashtriya Swasthya Bima Yojana (RSBY) and other state insurance schemes emerged in 2008-’09. The government became a bulk buyer of insurance for all people below the poverty line in a particular state. The government negotiated very low premiums, something like Rs. 500-600 per household at the time, but there was a huge growth of insurance in terms of volume. The premium is much higher now. So the RSBY in fact gave a boost to the private health sector because, one, all this premium went to the private insurance companies, and two, 80% of hospitalisations also happened in the private hospitals.

But did that at least mean access to free, quality healthcare for the poor?

Well, the RSBY provided insurance cover of Rs. 30,000, which did not cover tertiary care (highly specialised treatment like intensive care units or advanced surgical procedures like neurosurgery, organ transplant, etc.). It only covered secondary care like simple surgeries, etc.

Later, in 2018, the Pradhan Mantri Jan Arogya Yojana (PM-JAY) was launched on the basis of the experience of states like Karnataka, Tamil Nadu and Andhra Pradesh, which were the leaders in insurance-based programmes. But within a decade, these and other states realised that insurance was a fraud when first, there were cases of non-essential surgeries being done to claim insurance benefits came to light, and then, there were other instances of fraudulent activities. A lot has been written about how public insurance policies actually did not benefit people as they were supposed to and definitely did not reduce out-of-pocket spending. The PM-JAY is basically subsidising the private sector.

Why did out-of-pocket expenditure go up if insurance companies were paying for healthcare?

Out-of-pocket expenditure has always been high in India. Even to utilise the public health facilities for hospitalisation, the public has to spend out-of-pocket. Because the government hospital would say: sorry we don’t have the medicine, so take the prescription elsewhere. Our X-ray machine is not working, so please go out and get it done elsewhere.

The public system has generally lost its credibility over the years. And when you go to the private sector, they will tell you this is not covered and that is not covered [under the policy]. And as a result, people end up spending out-of-pocket. Then there’s also the fact that as people’s incomes rise, they have some surplus. When somebody falls ill, they use private facilities instead of going to public facilities because they know that doctors may not be there or medicines may not be available. So might as well use expensive private services instead of wasting time.

If you look at National Sample Survey (NSS) data, you can see that out-of-pocket expenditure is four to five times higher in the case of private facilities because the base cost which the government bears gets added on in private care. There’s adequate evidence from the NSS in the last decade or so showing that in states that rabidly implemented insurance-based models, out-of-pocket expenditure went up. This was the case even in states having good public health systems, such as Tamil Nadu, where the primary healthcare system is one of the best in the country. Yet, they had a state scheme that was insurance-based and the RSBY (which later became PM-JAY) on which they were heavily dependent on for tertiary care. Tamil Nadu tried to extend these schemes beyond the below poverty line (BPL) by adding its own resources. The 75th round of the NSS clearly shows us that out-of-pocket expenditure went up in Tamil Nadu too.

I always say that if you operate schemes, you will scheme.

Even though all these funds are publicly financed health insurance schemes, people are forced to go to the private sector.

So, who benefits from public sector health insurance?

There is a class of people, about probably 15% of the population, that earns well and also gets good social security—people working with the Central Government, our honourable members of Parliament, all the ministers—they all get the Central Government Health Scheme (CGHS) benefits. The government spends Rs. 8,500 per capita under the CGHS. But for the aam janata through the Ministry of Health, the government spends Rs.1,600 per capita. That’s the difference. So naturally, under CGHS people get good care; they get all the medicines, all the procedures, all the diagnostics, and they can even access private hospitals.

And the CGHS doesn’t disclose where exactly its budget goes. I’ve even put in an RTI inquiry to ask where the CGHS money goes. How much of it is outsourced and who benefits from that outsourcing to large private hospitals.

There’s discrimination even in that kind of a programme—those who are at the director level and above have a different rate of reimbursement than those who are the clerical cadre or white collar. On the other hand, defence services also spend about the same amount as CGHS, maybe Rs. 9,000 rupees per capita, but right from the jawan to the general, it is the same benefit. Same thing with the railways. So, these are good examples of good healthcare being provided.

Now if good healthcare requires Rs. 8,000 per capita, then that is what we need to allocate from the Health Ministry too if we want to run a robust public health system.

So there’s insurance but there’s still high out-of-pocket expenditure leading to indebtedness and poverty. What’s the point?

People with insurance policies were denied Covid treatment. We pushed the Maharashtra Government as part of the Jan Swasthya Abhiyan in Mumbai to start auditing private hospitals. They did that and about Rs. 15 crores has been refunded to patients who were overcharged by private hospitals.

Insurance is fraud: even in my own personal experience. When I was working, my employer paid my premium. I used to go to the dispensary if I needed outpatient care, but when I needed hospitalisation, I had insurance cover. So I decided to go to Jaslok Hospital because there was a surgeon friend of mine who was going to operate on me. They gave me a bill of Rs. 60,000, but the insurance company said sorry, we will only pay Rs. 45,000 and they paid the hospital since it was a cashless scheme. I had to pay the balance of Rs. 15,000 so that I could leave the hospital. I had a public sector insurance policy and I had to squabble with them for six months before I got another Rs. 10,000 back. I still had to pay Rs. 5000 out-of-pocket.

This is the case for somebody who considers himself a public health activist, who knows how the health system operates, or how insurance operates. I paid the premium for almost 15 years and then had to struggle to get my money back.

Is it a problem of consumers not knowing how health insurance works or how to reap its benefits or is it a structural problem with how insurance works and what the terms are?

I think the problem is less with insurance, and more with the lack of regulation of the private sector and the lack of ethics in practice. When doctors are not ethical and encourage unnecessary tests, insurance becomes defensive. They question everything. There’s no standardisation of treatments protocols, and that is why there is a gap between the insured and insurance and the hospital.

When I was pursuing my reimbursement, the insurance company told me upfront that Jaslok charges 30% more than what they should be charging. So, when we reimburse, we just knock off 30% off the bill. If you had gone to some other hospital, we wouldn't have deducted anything. This means the insurance companies should put out a notice saying please don’t go to Jaslok and Breach Candy, instead go to [such-and-such] hospitals, then you will be reimbursed!

So assuming the information was out there and private players were made to adhere to it, then would health insurance work?

Look, in PM-JAY, they have defined protocols—this is a list of things that are covered and this is the cost that we will pay. There are huge frauds even in that. If I have a Rs. 5 lakh cover in a year, which is for all the family members, what the hospitals do is target your policy. They will do all kinds of things to see that you use the maximum amount of your cover. A lot of overcharging happens and our audit systems are very poor. Insurance companies don’t have a separate audit mechanism and even the third-party administrators that are supposed to help with that are very weak in terms of auditing private hospitals. Distrust builds on all sides.

I think health insurance has no future in this country or anywhere in this world. Global experience tells us that insurance doesn’t work anyway.

The United States is the only example of a country that uses insurance in a major way and we know it’s a disaster—the insurance companies call the shots and they now own hospital chains. The doctor in a hospital has to call the insurance company and get advice. The insurance person may not even be a doctor and they’ll say no you can’t do this procedure, so you do this instead.

The private sector is here to stay though, isn’t it? Is there no way public-private partnerships (PPP) can work in the health sector?

Experience shows that they don’t work in India because a public-private partnership (PPP) for the public sector means abdication of responsibility and for the private sector, it means milking the state. They get their assured profits, but there’s no guarantee that the services will be provided by them in an optimal manner. Except for perhaps ambulance services, PPPs have been an utter failure.

There was a PPP for the Revised National Tuberculosis Control Programme (RNTCP) in the 1990s in which the government involved the private practitioners. The government said that we will pay you Rs.2 for the simple task of administering the drug to ensure supervised provisioning of medicine. People would come to the clinic, they would be given that tablet which the government provided free, a glass of water and the patient was supposed to take it in front of them. That was all the time that the doctor had to give and they negotiated with their association that there will be so many patients guaranteed who will come every day and this is what the payment would be. But then these doctors started charging patients whatever the outpatient department (OPD) charge was: Rs. 30, Rs. 40, etc.

Practically speaking, what can the government really do?

Regulate the private sector, including what prices they charge. But the government should not develop PPPs, or develop programmes that ultimately benefit the private sector. Instead, the Rs.6,400-crore-budget of PM-JAY (2021-’22) should go into strengthening the district hospitals and system. The government actually has a policy of converting every district hospital into a teaching hospital. But the Niti Aayog says: do it in the PPP mode, which basically means giving away the district hospital to a private entity. That should not happen. Get money from elsewhere to do it. Use CSR (corporate social responsibility) funds, or mining mineral development funds, or forest funds—huge accumulated funds that the government is using to pay salaries because tax collections have come down during Covid.

As for insurance, let private insurance operate in the market.

Why do they need the crutches of the government? If you believe in the market, then operate in the market. It will bring down their insurance premiums substantially.

And what should people do? Should they buy health insurance?

I teach a lot of public health courses and what I tell young people is: don’t buy insurance. When you are young, the chance of you having a medical emergency is low. So if you start saving from the moment you start earning, and put a certain amount in a recurring deposit, the capital will be yours and in time, the income or interest on that capital will also be yours. And when you need it, at least the money will be there. Otherwise, the health insurance company will eat up your capital every year and you won’t get anything back [as you would in annuity-based policies or money-back life insurance policies]. Insurance design is bad in India. You can’t claim insurance for consultations as in the United States. Our insurance mostly covers hospitalisation and even then, there are exclusions.

It is a design that accumulates your money for their profit.

Now when you become older and stop earning, who will pay your premium when you most need healthcare? You would’ve given away so much of your money to insurance companies and they’re not going to give it back to you.

What about the “what if” scenario that is compelling enough for most people to buy insurance? If I incur an emergency medical expense and I only have my premium as savings (even if it is for several years), those savings will not be enough to cover my bills. In fact, I might end up exhausting those savings and some more. Insurance, on the other hand, might at least cover a big chunk of it.

So, what I’m suggesting is a two-pronged strategy. First, you accumulate your money and use this only for medical expenses. Now there is a chance that 1 out of 100 people may have an emergency and not have enough money accumulated. And yes, that is a risk. But the majority would accumulate enough and that’s why I am suggesting this.

The second thing that must go alongside this is that, as the middle classes, we need to use the public health system. It is more or less free. If we use it, we will improve the quality of the system.

We will shout, we will make our presence felt, we will call them out, we will ask for accountability. The poor are unlikely to do all this. Because we have neglected the public health system by not being users, we are also paying the price by having to buy insurance.

I would support something like accident insurance though. Especially in these times, and if you are living in a metropolitan area, the chances of meeting with an accident are quite high. And accident insurance is relatively quite cheap.

Talking of money, budgetary allocations for health receive much attention each year in the news. If we were to increase the expenditure what would your top three choices be to put that money into?

I would say strengthening primary healthcare. The Health and Wellness Centre concept in Ayushman Bharat is a very good concept, provided we can get the personnel and the medicines etc., to run that. Basically, the sub-centre, which is there today with one ANM (auxiliary nurse midwife), should be upgraded with maybe another ANM or a male worker and a mid-level health care provider. It could be someone who can provide the first level of primary care, even Ayush practitioners. Anyway, the NSS tells us that 95% of Ayush practitioners actually practise allopathy. That’s the first thing, and that will require at least 60-65% of the budget. We’ve done these calculations for Maharashtra and for Chhattisgarh as well.

Next, we need to strengthen the district hospitals, because that’s our key tertiary care point. This can be done by converting all the district hospitals into teaching hospitals, not with PPPs, but by the governments themselves. If you do that, then there’s less of a burden on the community health centres or sub-district hospitals. Good sub-district hospitals can provide secondary care with simple hospitalisations that may happen at that level.

And for ambulatory care (medical care on an outpatient basis, without hospital admission), we should develop an NHS (UK’s National Health Service) kind of system. If you can’t get people to come and work on a salary, then sign contracts for at least ambulatory care, especially in urban areas. In rural areas, you may get mid-level providers. For example, in Chhattisgarh, they have a surplus of 8,000 dentists who are unemployed. So they are going to use dentists as mid-level providers. Dentists anyway get allopathic training and then people can also get dental care, which is a very neglected area.

What would you say is an ideal number as a percentage of the GDP?

The government says we’re at 1.6-1.8% right now, but that is including water supply. Water supply is not the mandate of the Ministry of Health, so it shouldn’t be included. Moreover, you should also deduct ESIC (Employee State Insurance Corporation) and CGHS because the aam janata doesn’t benefit from them. So, after making these deductions, expenditure on health is probably around 0.8% of the GDP.

To begin with, at least let’s honour the health policy commitment of 2.5% of GDP and double our expenditure in one go, and not wait for five years.